.svg)

A Lack Of Freshness Spoils Returns

Alpha Theory can’t tell you how to do your research, but it can tell you when. Using insights from the Alpha Theory All-Manager dataset, we can provide guidance on some of the basics in managing your research process.

Alpha Theory can’t tell you how to do your research, but it can tell you when. Using insights from the Alpha Theory All-Manager dataset, we can provide guidance on some of the basics in managing your research process.

Managers understand intuitively that producing investment research and updating that research regularly (i.e. freshness) is important. But how frequently? Should I update my research every 60 days? Every two weeks? Do I need to produce scenarios for all my positions?

Key conclusions:

1. Assign price targets and probabilities to every investment

2. Update them once a month

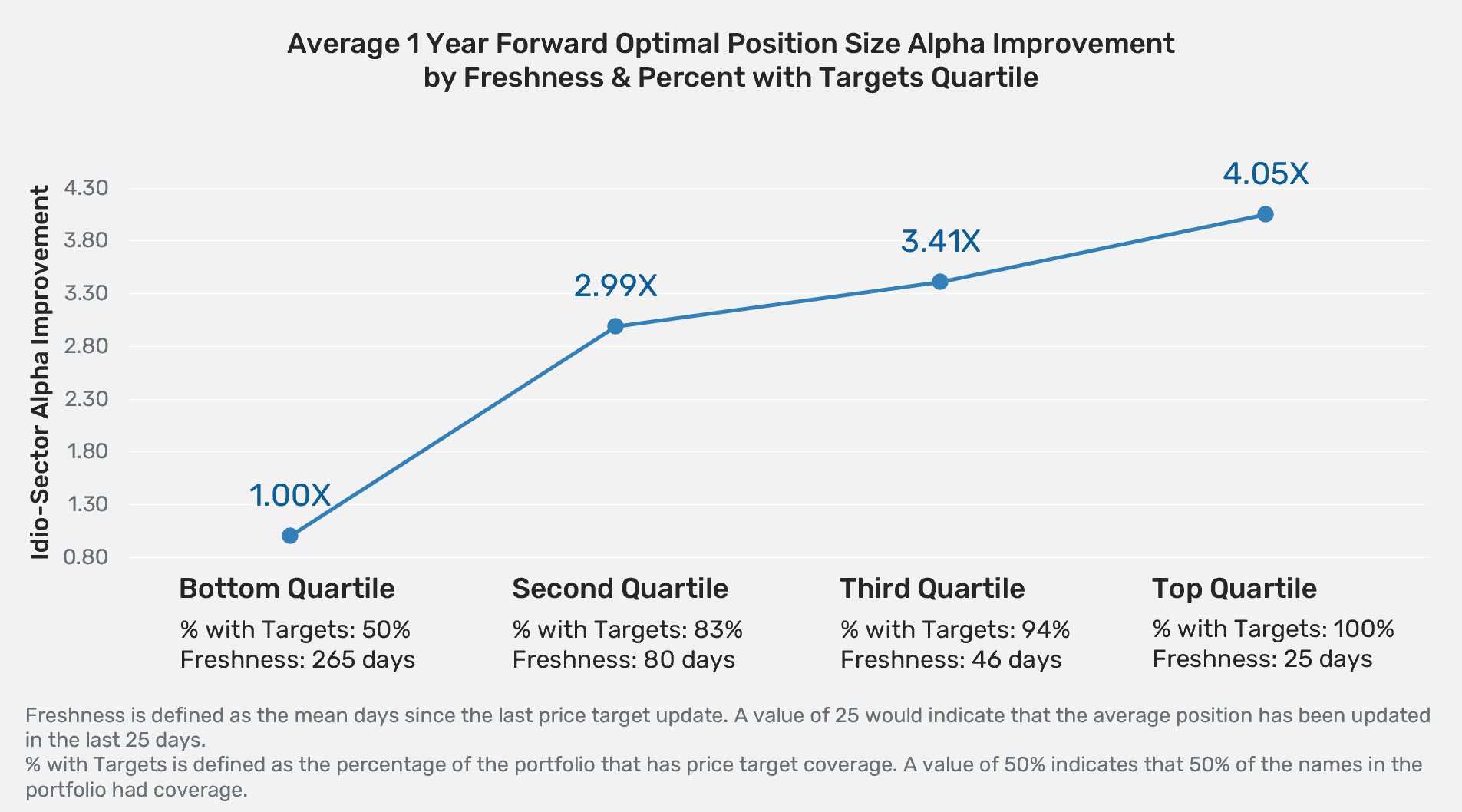

To determine the impact of freshness and coverage on returns, we measured the one-year forward return for the optimal long portfolio for each fund in the Alpha Theory All-Manager dataset on a quarterly basis1. We then put each fund into four buckets based on their average freshness (days since the last price target update) and coverage (percentage of positions with price targets). Next, we calculated the return of each quartiled bucket to see if returns correlated to freshness and coverage.

We found that funds that were diligent enough to place in the top quartile produced more than four times as much alpha as the bottom quartile, increasing monotonically from bottom to top. The median update frequency for the top quartile was 25 days (once a month updates), meaning the top funds updated more than 10x as often as managers in the bottom quartile. Additionally, managers in the top quartile had research on all active positions.

As a fundamental manager, you may argue that very rarely does something meaningful happen every 30-days that warrants a forecast update. We would counter that price is an important signal. For example, let’s say you initiated coverage on a position at $100 with a 70% chance of going to $150 and a 30% chance of going to $50. If the price moves from $100 to $125, wouldn’t you say the probability of reaching your bull target has changed? While $150 may still be the price suggested by your model, updating the probabilities of your scenarios to more accurately reflect likely outcomes allows the OPS model to make better sizing recommendations.

In addition, Daniel Kahneman’s new book “Noise” describes how the same expert can take the same information and come to different conclusions at different times. And, that the best answer is the average of those forecasts. This means that an analyst may come to a different conclusion for price target and probability on a different day and that the constant refinement (updating once a month) is healthy and leads to more accurate forecasts.

Finally, research from our friends at Good Judgement Inc. shows that over the past six years, their top forecasters (orange) update roughly 4x as often (11 updates vs 3 updates per question) as non-Superforecasters. Update frequency has a high correlation with outperformance and incorporating even small additional bits of information (Superforecaster updates were roughly half the size of non-Superforecasters) that either support or detract from the probability of a given outcome lead to better results over time.

We are always interested in learning more about your research process and where Alpha Theory can help. Alpha Theory is a process enhancement tool, creating a space that systematizes how you conduct and use research for allocation decisions. Please reach out to us with any questions so we can better optimize your workflow to generate more alpha.

1To normalize for different benchmarks, we calculated alpha on an idio+sector basis using the Axioma World-Wide Equity Factor Risk model, which removes performance derived from all their tracked factors, excluding sector.