.svg)

Why Price Targets Are Broken And An Easy Method To Fix Them

In this article, Cameron Hight relates price targeting to poker. Great poker players calculate price targets by determining the amount of money in the pot and determine the probability of winning the pot. Read more on his thoughts here.

I used to carefully calculate a price target for every asset I invested in. I was, after all, a sell-side analyst for many years and the price target was a staple. But when I used price targets to actually deploy capital, I was less than satisfied. I always had a nagging feeling that something was missing. It took reading a book on poker theory to wake me up.

Great poker players calculate price targets by determining the amount of money in the pot. But they do not stop there. Great poker players determine the probability of winning the pot and combine that with pot size and the amount they have to bet (risk) to determine a probability-weighted return (i.e. if they were to play the exact same hand situation 1,000 times, the return they would expect). Why wouldn’t I do the same thing for every investment I make? Take my price target and combine it with my estimate of downside risk and multiply each times my best guess of the probability of each event occurring.

Yes, the probability of winning a hand of poker is different than determining the probability of a stock going from $20 to $40. Poker has aleatory probabilities, which means they are defined by observable statistics and investing has epistemic probabilities meaning that probabilities cannot be determined by historical observation (these are words learned from listening to Ronald Howard, Stanford Business School professor that has studied decision making for the last 40 years). Investors describe the same aleatory and epistemic probabilities with different definitions. Definable probability is called risk, and an indefinable probability is called uncertainty. Uncertainty does not mean we should not use probability, because we are using our “confidence” to influence the investment decision anyway.

Gene Gigerenzer describes it like this in his book “Calculated Risk”, “Degrees of belief are subjective probabilities and are the most liberal means to translate uncertainty into a probability. The point here is that investors can translate even one-time events into probabilities provided they satisfy the laws of probability – the exhaustive and exclusive set of alternatives adds up to 100%. Also, investors can frequently update probabilities based on degrees of belief when new, relevant information becomes available.”

Many firms have a spreadsheet with price targets for each stock in their portfolio. Their price target represents the value the stock should achieve assuming their thesis is correct. But what if their thesis is wrong? Their price target assumes a 100% probability that their thesis comes true. If that is not the case, then downside risk has to be part of the equation. And if the chance of upside or downside is not a coin-flip, then probability must be assessed. These are the metrics that an analyst should be trying to tease out of their fundamental research because they describe the true expected payoff from the investment. Price target does not give you a probability-weighted return! Anything less than a probability-weighted return requires you to rely on your mental calculator to combine profit, risk, and conviction level.

Price Target is the most common measurement used by fundamental money managers to evaluate asset quality. The Price Target represents an analyst’s best estimate of value and is a synthesis of their research. The Price Target is then compared to the assets current price to determine if there is a significant enough dislocation of value to provide the fund an opportunity to profit. The Price Target is dynamic because it can be adjusted as the analyst receives new fundamental data. It can also be used as a trading tool that notifies the fund when to enter and exit positions.

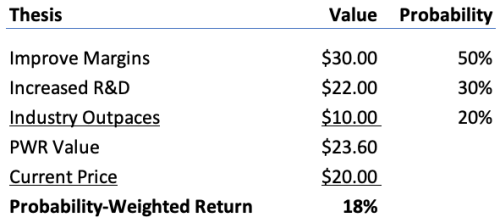

For all of its attributes, one inherent flaw has made Price Targets impractical for money managers. Price Target only explains the most likely scenario and thus assumes a 100% probability of its outcome being true. For example, Company ABC is trading at $20 and has just hired a new CEO who is known for cutting costs and improving gross margins. Company ABC has historically had margins and multiples below industry norms. So, in your Price Target, you give the company the benefit of industry margins and multiples and determine the company should be worth $30. This is an implied return of 50% and sounds like a solid story. However, the company is a generation behind in product development, so it may be difficult to generate equivalent margins and the company may have to spend on R&D to catch up with the industry. Additionally, there is an even riskier scenario that the industry continues to outpace Company ABC in product development and their competitive position actually disproves to a point where margins are severely impaired. Maybe these other outcomes are not as likely, but they must be accounted for in the measurement of asset quality.

This is where many portfolio managers will assess that the asset has great potential upside to $30 from $20, but there are substantial risks that prevent the fund from taking the exposure that generally would be given to an asset with 50% potential return. In this method, the portfolio manager was forced to use heuristics and mental calculation to adjust for risk. But why force yourself to be a human computer when you have all of the relevant information to make a more accurate decision? The first step is to appreciate that the firm’s thesis does not have a 100% probability of occurring. Once a firm indoctrinates that tenet, it is easy to see that all 50% return assets are not created equal.

Let’s use our Company ABC example to fully describe the asset using the analyst’s research. The thesis is that the new CEO will improve margins and the company will receive a multiple in line with the industry. The analyst believes there is a reasonable chance that this occurs, say 50%. The analyst also calculates that if the company was forced to spend more on research and development to catch up from a product standpoint, the stock would be worth $22 and this has a lower chance of occurring, say 30%. Lastly, the chance that the industry advances their lead on Company ABC’s product, severely impacting margins, is about 20% and would probably take the stock down to $10. We have now described the full breadth of our research and we can synthesize it without heuristics or mental calculation:

The 18% Probability-Weighted Return (PWR) explains the full breadth of your research, is an accurate measurement to make portfolio decisions and is an apples-to-apples comparison of all assets. But this is just the beginning of the benefits of PWR because assets are now being measured by how much return you gain for a given level of risk.

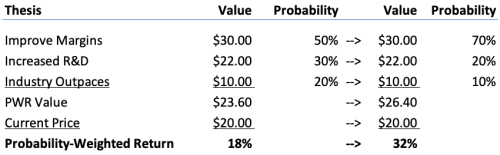

We will continue with our analysis of Company ABC. The analyst is in San Francisco and has just exited a one-on-one with Company ABC’s CEO. He finds out that product development is going ahead of plan at a lower cost and the product should be industry-competitive in the next few months. Let’s evaluate how Price Target and PWR would each deal with this new information. For Price Target, things are going according to plan so we wouldn’t raise our target above $30. With PWR we can confidently assess that our probability of success has increased and our probability of overspending on R&D and falling behind the competition has decreased. We would quickly adjust our assumptions:

Using PWR we see exactly how much better our idea is given the new fundamental data and can easily see how much better the position is than it was before. The portfolio manager can be confident in adding to the position and have a sense for how much.

The process is so much better using Probability-Weighted Returns. Using Price Targets is certainly better than guessing, but it leaves important information needed to make the right decision. If you’re using Price Targets today, take the time to reassess your approach. Start with downside targets with fixed probabilities (50%/50%) and then, over time, add differentiated probabilities to get the full impact of Probability-Weighted Returns on your portfolio.

.png)